Are you considering longevity risk within your strategic journey plan?

Pensions & benefits

Many UK defined benefit pensions schemes are now closed, either to new members or to future accrual as well. They have a finite lifespan and are now focussed on how best to ensure they can meet the promises that have been made to their members.

LCP’s Strategic Journey Planning framework and Chart your own course series of reports helps trustees to strategically navigate their scheme’s journey. Schemes are creating plans to reach their long term objectives, such as a low dependency basis or full buy-out.

The targeting of such a long-term funding objective for closed schemes is a key plank of the Pensions Regulator’s Scheme Funding proposals.

Step 3 of our Strategic Journey planning framework is about understanding what could change your journey, and longevity risk is a key part of this. For many pension schemes targeting a low-risk investment strategy, the risk of members living longer is, or will be in the future, their dominant risk and it should be factored into journey planning.

Pension schemes looking to manage their risk budget in the most efficient way will reduce risks in parallel to maximise diversification benefits. However, many schemes either ignore or do not address longevity risk, leaving them with a poorly defined or unbalanced set of risks.

Typical risk profile for a £1bn pension scheme with ongoing investment strategy

Typical risk profile for a £1bn pension scheme with low-risk investment strategy supporting long-term funding target

How can you manage longevity risk?

There are two main ways of hedging longevity risk:

- Buy-in transaction with an insurance company. In return for an up-front premium the insurer will agree to meet all pension payments for a defined group of members. This hedges all longevity and investment risks.

- A longevity swap. A reinsurer agrees to pay pension cashflows for a defined group of members while the pension scheme pays the reinsurer an agreed, fixed set of cashflows. This essentially swaps the longevity risk to the reinsurer (in a similar way to an interest rate or inflation swap). This option is mainly available to larger pension schemes, and are typically structured through an insurance intermediary or captive arrangement.

In practice, the cost of hedging the longevity risk is the same under either route. UK life insurance companies reinsure the vast majority of their longevity risk due to the capital benefits under their insurance regulatory regime, so in practice reinsurer pricing determines the ultimate pricing benchmarks.

How is Covid-19 affecting longevity pricing?

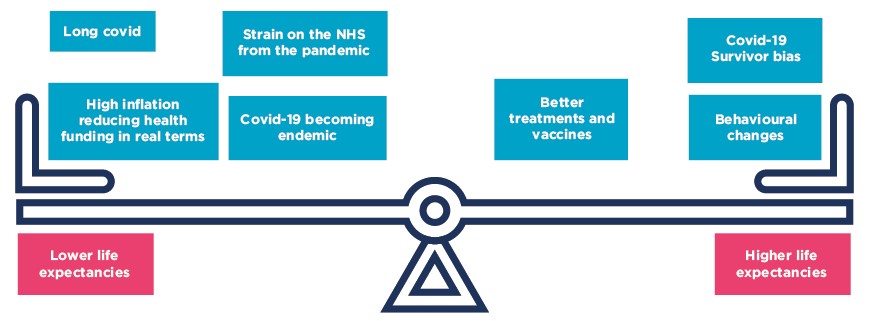

While mortality rates increased significantly through the Covid-19 pandemic, reinsurers were initially cautious about passing on pricing adjustments to pension schemes and insurers. Partly this was driven by caution, though there are factors which could cause life expectancies to increase or decrease and insurers were considering which way the balance would tip.

Supply and demand dynamics

While pension scheme demand for de-risking products continues to grow, there are strong supply-side factors putting downward pressure on pricing. In particular:

- Recent new entrants are providing competition and capacity for longevity reinsurance. There are potentially 15+ reinsurance counterparties actively operating in the market.

- There is a strong rationale for reinsurers to take on longevity risk to diversify and balance their overall risk profile. Many hold large books of mortality risk from life assurance products (particularly US whole of life assurance) which has been hit by losses from Covid-19. Longevity risk provides an important offset and/or diversifier to this risk.

- Potential changes to solvency II may allow some UK insurers to hold higher proportions of longevity risk without incurring associated penal capital charges. This may help support market capacity.

Over the longer term, there are questions over ability of the reinsurance market to absorb increasing demand from pension schemes at current pricing levels.

Read more about longevity risk with practical guidance in our latest longevity report.