Inflation from an unlikely source - should we care about container shipping?

Investment

For many of us, buying things online is now routine. We fill in name, address and so on, and then the stuff magically appears several days later at our front door. It just works, and we don’t usually think much more about it.

For the products themselves though, this is often the end of a multi-thousand-mile journey through the global container shipping system. Combined with the internet, container shipping has helped revolutionise where and how goods are made, and how they are bought. These in turn drive efficiencies of scale, allocation of capital and resources, greater choice and perhaps has ultimately helped keep inflation in check over recent decades.

With the recovery from the Covid-induced crisis now well underway, inflation risk seems to be the theme of the moment. The big concern is that a sharp upward move in inflation could cause central banks to raise interest rates faster than what’s anticipated currently. This could cause volatility in financial markets in a similar way to talk of tapering QE back in 2013.

Inflation could come from many places – both traditional and new, and this is something we’ve been discussing and debating since the beginning of the year (more here on the two broad schools of thought regarding inflation).

But should inflation-wary investors now also be worried about the impact of container shipping? First, let’s have a brief look at what’s been going on in the world of container shipping this year.

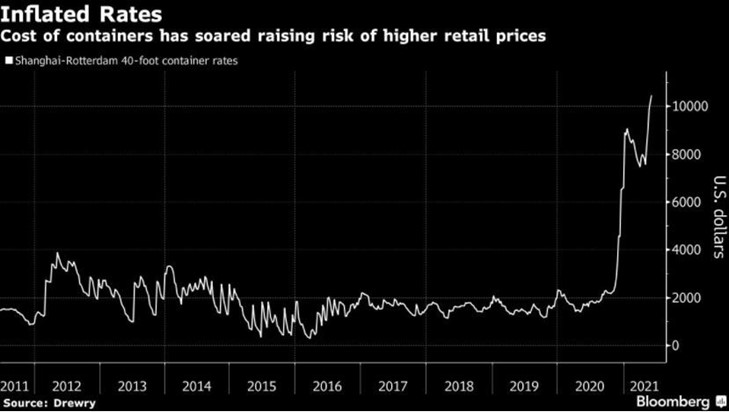

In brief: The problems (and price rises) in container shipping

The price of container shipping has ballooned in recent months. For example, by 500%, from around $2,000 to around $10,000, to ship a container from Shanghai to Rotterdam.

A shortage of physical capacity and labour, driven by ongoing measures to contain Covid-19, and a huge demand for shipping as economies recover seem to have damaged the smooth operation of the business of shipping. The Ever Given crisis in March certainly didn’t help either.

Used with permission of Bloomberg Finance L.P.

In particular:

- Port congestion, capacity constraints and labour shortages are leading to material delays in unloading and loading container ships, and even the re-routing of voyages. This in turn has discouraged ships from waiting in ports to be re-loaded with empty containers for the return voyage.

- This leads to too many containers being in the wrong place – ie too many empties at importing ports, and not enough at exporting ports. This adds to port congestion and inefficiency, but also leads to:

- A global shortage of the metal containers themselves, in the places where they are needed. More are being made, but over 80% of the world’s containers are made by just three companies, and given these market dynamics the price of a new container itself has also risen, from around $2,000 in 2019 to around $3,500 this year.

These effects seem to be forming a vicious circle that has moved container shipping rates up rapidly. And there seems to be no end in sight yet - only last month, tighter Covid-19 restrictions brought in to combat the delta variant are impacting major container ports in Guangdong province, China.

There have also been some questions asked of the shipping companies themselves and why competition between them hasn’t arrested this increase in prices. These may be investigated in due course, but this won’t do anything to help businesses looking to move goods around the globe at present, and all the while the more basic, operational issues listed above are in plain sight.

A traditional view seemed to be that “shipping costs don’t matter much to price inflation, because shipping is such a small part of the overall expense of goods, and it’s a small element of the many factors that drive price inflation".

But does this still hold in the face of such large increases in shipping prices? Last month saw news that:

- The Entertainer, a UK toy shop, had to stop importing giant teddys as their retail price would have to double to cover current freight costs;

- Peppermill Interiors, a Midlands furniture supplier noted that an armchair which used to cost £12 to bring in from China now costs £100, and so the retail price has had to be increased by 25%.

These are clearly super-micro examples in the overall price inflation picture. But more broadly, some recent work by HSBC estimated that a 200% increase in container shipping costs over the past year could raise euro-area producer prices by as much as 2%.

This wouldn’t be a step-change in inflation, but it’s an inflationary contribution from an area that has perhaps been more likely to keep prices in check historically.

The “drivers” of price inflation are always multiple and interlinked – labour market conditions, national government fiscal policies and central bank monetary policies are likely to remain centre stage in the ongoing debate around inflation. Furthermore, the policy response to a burst of inflation (or “reaction function” in the jargon) is often as important as the underlying economics causing it in the first place, and this often hinges on whether inflation can be viewed as transitory or here to stay.

Many smart-sounding theories have been turned on their head as the unpredictable nature of these complex interactions can end up with the opposite effect to what you initially think, so a dose of humility is needed in trying to make predictions.

But I’ll certainly be keeping an eye on the container shipping industry, which looks set to continue to add upward pressure to the prices of goods imported around the world, and I expect we’ll hear a lot more about this in the coming months.

Finally, watching and worrying about inflation indicators is one thing, but what can investors actually do to insulate themselves and maintain the real spending power of their investments? We discussed a wide range of ideas here, though as we go on to explain, none of them are a straightforward solution at all.