Market evolution and consumer need will drive Home Energy Management system sales growth as 2.4 million installed in 2023 – LCP Delta

Energy transition Residential research Net zero

In their latest analysis of the Home Energy Management systems market, LCP Delta has highlighted that over 2.4 million HEMS were installed in 2023 across Europe, and more HEM companies are now looking to integrate their products or expand their market.

A Home Energy Management system (HEMS) is a system that monitors, controls, and optimises energy generation, storage and consumption within a household. They are used by consumers to help them track and optimise energy consumption and minimise costs.

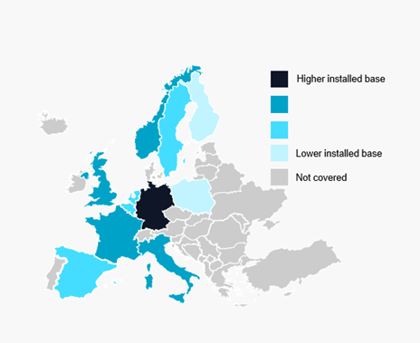

While Germany remains the leading European market for HEMS because of its large base of solar PV and battery storage, the UK is the second largest market. Key drivers are high electricity prices, increasing deployment of connectable electrical assets in the home, process and the liberalisation of electricity market mechanisms.

The European HEM and Appliance optimisation market is expected to accelerate in the upcoming years, reaching over 7 million annual sales by 2030. This growth is mainly due to an increasing number of large electrical assets being installed in European homes, new players offering optimisation services, market and technology expansion from existing solutions, and increasing partnerships allowing different assets and brands to be optimised by various solutions, including EV charge points to and heat pumps.

HEMS and Appliance Optimisation systems installed base by 2023

The analysis highlights the key emerging trends in the market.

- The installation of large electrical assets continued to grow in 2023, and the overall annual sales of large electrical assets grew in 2023. However, the market growth was not uniform, with some assets, such as heat pumps and hot water tanks, suffering a slight decrease in sales.

- The HEM market continues to be very dynamic. Over 140 HEM and Appliance Optimisation offerings exist across Europe, with new entrants and existing players evolving their HEM solutions.

- A strong trend in the last year has been the development of partnerships in the HEM space as stakeholders strive to integrate more assets and unlock additional value streams. More existing HEM providers are partnering with equipment manufacturers (OEMs) to expand the portfolio of assets that can be integrated into their HEM platforms.

- While HEM providers/OEM partnerships are helping to overcome interoperability issues between assets and HEM platforms, this remains a significant barrier to market growth. There is no clear standardisation among the protocols used by HEM-related asset manufacturers, and the development of common standards would accelerate market growth above LCP Delta’s forecast. While this does not appear likely in the short term, successful HEM platform / OEM partnerships combined with revised grid regulations could together contribute to a more open and standardised market.

Ricardo Lopez, Home Energy Management Research Manager at LCP, commented:

“Consumers wanting to get smarter with how they consume their energy and the growing deployment of heat pumps, solar panels, and other large electrical assets are helping to drive the rise of the HEM market. As the transition to renewable energy sources continues, there is room for substantial growth across European countries.

“However, while we see an increase in drivers, there are some barriers to growth across different markets, such as slow smart meter rollout, poor interoperability, supplier tariff structures, subsidies being removed, and uncertainty about regulatory direction.”