It’s fair to say there is a lot going on in the pensions industry at the moment, with packed agendas and a lot of hot topics to get your head around.

But there are two questions that are likely at the top of the list for many trustees and sponsors:

- how to best fund the pension scheme; and

- how to ensure a successful journey plan to your long-term target, managing risk along the way.

To me that means contingent funding solutions should be high on the agenda at upcoming valuations, and in many cases even sooner.

Ask the obvious questions

But first it’s important to ask the obvious questions: what’s the point of contingent funding? After all, isn’t everyone better off if the sponsor just pays in the cash the scheme needs?

In many cases cash might be the right answer – for example where a scheme is poorly funded with a strong and cash-rich sponsor.

But what if the sponsor can’t afford the payments, for example because it’s been hit really hard by Covid-19, or just has an overwhelming need to invest for the business?

And at the other end of the spectrum what if the scheme is already well funded, and the sponsor is reluctant to pay contributions unless there is a chance of getting them back if they prove to be more than enough? We are already seeing some schemes with more than enough assets to secure their liabilities, and no CFO wants to be responsible for over-funding their pension scheme.

Even for slightly less well funded schemes, there are some who want to rely only on the longevity of the sponsor covenant and investment returns, without paying any more cash unless things go worse than expected. But covenant can change quickly as we’ve all seen, as can the size of the scheme deficit, not to mention developments in the regulations on scheme funding.

Contingent funding approaches can address all these concerns – and importantly can deliver a win-win outcome for both the sponsor and the trustees.

What do we mean by contingent funding?

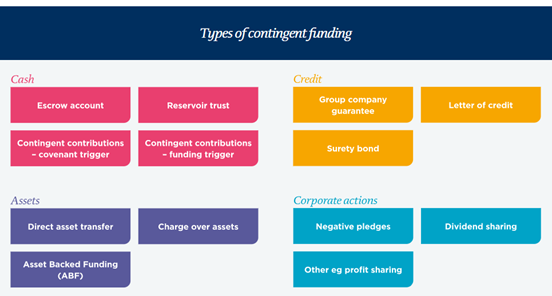

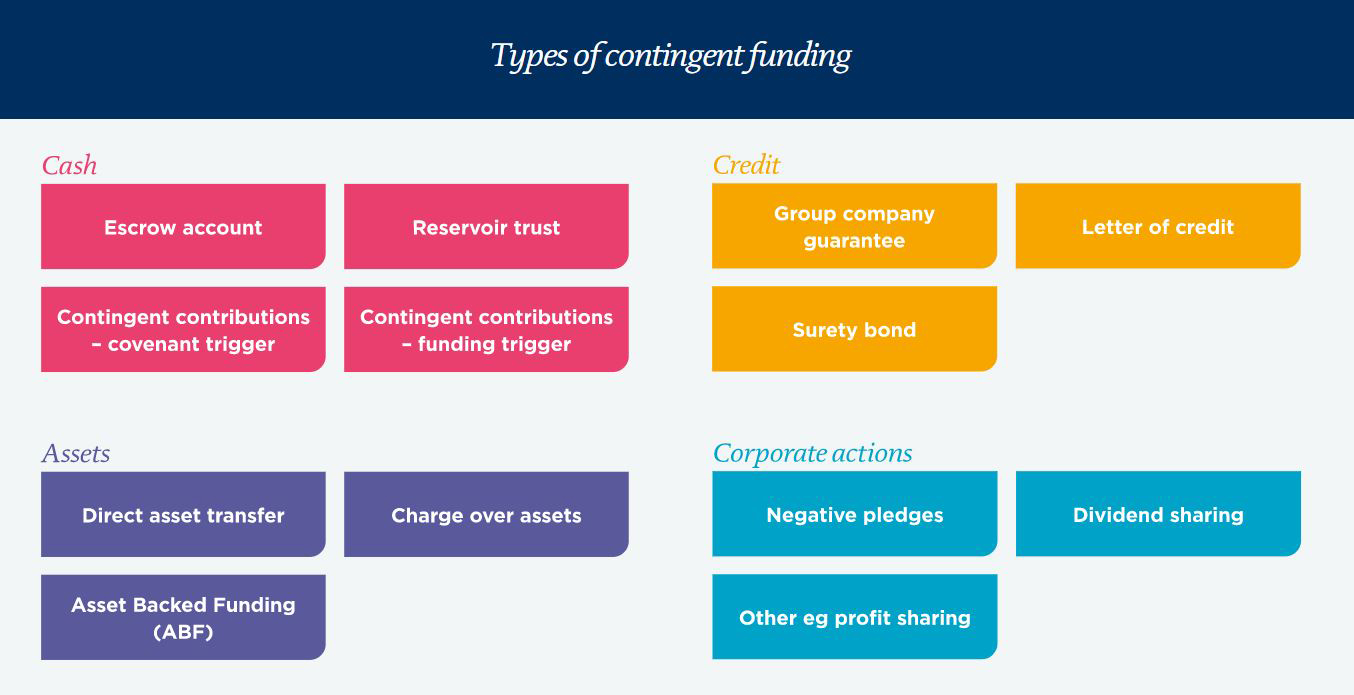

Contingent funding incorporates a wide range of measures that can be used to provide support to a pension scheme. The chart below shows a summary of some of the most common types.

Escrows in particular are increasingly popular thanks to their flexible nature and ability to satisfy many different objectives. For example they can be used for additional covenant support or as security for contingent contributions; they can act as a buffer where there are different views on appropriate valuation assumptions; or they can help to avoid trapped surplus and the hefty 35% tax charge due on a refund of surplus at wind-up.

Another popular solution is an Asset Backed Funding vehicle (ABF). This is probably the most complex of these vehicles, but in return for that complexity you can get lots of benefits. Sponsors can see a longer recovery plan and hence improved cashflow, option for a switch-off trigger to manage overfunding risk, and – subject to certain conditions – an accelerated tax deduction on day one. Trustees get enhanced security, perhaps some covenant diversification, and a reduced headline deficit from day one as ABFs are recognised as a scheme asset.

You can find out more about all these types of solutions and how they can be used in practice in our interactive contingent funding handbook.

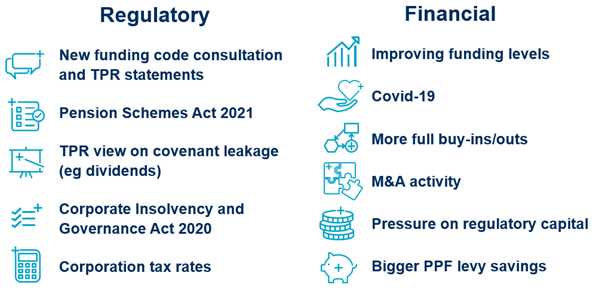

Why is it becoming so important?

Well, for lots of reasons. Below is a quick summary and each of these is easily worth a whole blog by itself (if you want to learn more about any of these topics, you can also find that information in our handbook).

Without going into any detail here, you can see there are a lot of different drivers, so it’s no wonder so many of our clients are engaging with contingent funding.

At our recent webinar covering the latest in contingent funding, more than half of survey respondents said they are considering introducing new contingent funding approaches for their pension scheme – with escrows, reservoir trusts and ABFs being the most popular solutions. And we fully expect the popularity of contingent funding solutions to keep increasing.

Contingent funding in practice – from large to small

At that recent webinar we were delighted to be joined by Paul Rogers, the Pensions Risk Director at BT, who went through the package of contingent funding measures that BT negotiated recently with their trustees for the £55bn BT Pension Scheme.

The BT package included a £2bn Asset Backed Funding arrangement, a co-investment structure (with similar economic benefits to an escrow and a few key additional features), and contingent contributions in the event of negative funding experience and certain corporate events.

This really was a perfect case study of contingent funding in action, and how this can provide a great outcome for all stakeholders. And BT are not alone, we are aware of a number of other employers taking similar actions. All this proves that there is plenty of innovation in this space and there are sophisticated solutions that can be developed to the particular needs of larger schemes.

But it’s important to note that there is also growing use of off-the-shelf contingent funding approaches which can meet a wide range of objectives more cost-effectively, for any scheme size.

A great example of this is our Streamlined Escrow, which my colleague Katie Peto has previously written about here. This is quick and efficient to set up, helps provide certainty on fees, and has lots of flexibility – with different investment options, no minimum or maximum contribution levels, and no limits on the number of contributions or withdrawals that can be made to or from the escrow.

We’ve already had some great success stories from the Streamlined Escrow, and Katie spoke about some of these case studies during the webinar mentioned above.

What this all means is that I think some form of “win-win” outcome really is achievable in the vast majority of situations. That might mean a simple vanilla or off the shelf vehicle, or it might mean a highly bespoke one – the key is these solutions can be tailored to meet an incredibly wide range of different situations and objectives.