Urgent action needed to prevent retirement disability benefit timebomb - LCP

Health analytics Economy Impact Demographics

A rapid build-up of people spending a decade or more in retirement on disability benefits is on the cards unless urgent preventative measures are taken, according to new research from consultants LCP. Whilst much of the discussion around working age ‘economic inactivity’ has focused on those receiving benefits for those unfit for work, these benefits stop at pension age when recipients switch onto a state retirement pension. But disability benefits, such as Personal Independence Payment (PIP), continue to be paid into and through retirement for those who are already eligible when they retire. Unless action is taken to improve the health of these individuals, this new analysis suggests a risk of soaring benefit bills.

Key findings from the research include:

At present, there are just under 100,000 people aged exactly 66 (state pension age) receiving PIP or its predecessor benefit, Disability Living Allowance (DLA); on average, the paper suggests that such people are likely to draw benefit for another 11 years; total payments per person would be around £70,000 – and more if they are on a low income and claiming means-tested benefits as well.

Over half of the people on PIP at state pension age will continue claiming PIP until they die

Without action, the total number of pensioners on PIP/DLA is likely to rise by around 60% in the next decade from roughly 1 million now to 1.6 million in 2033; the total cost, in current price terms, would rise from around £6bn to £10.5bn

The total current cost of PIP in 2023/24 is £21.8 billion, and the benefit is paid to 3.2m people. The number of adults in receipt of PIP (plus DLA) has risen by around 1 million in the last decade and is forecast by DWP to rise by another million in the next three years. For younger PIP recipients, the fastest growing reported health condition is mental health problems, whereas, for older claimants, it is more likely to be musculoskeletal complaints. The fastest growing group of recipients is those who have been in receipt for five years or more, suggesting a risk of a large and growing ‘core’ of recipients with a dwindling prospect of flowing off benefit at all.

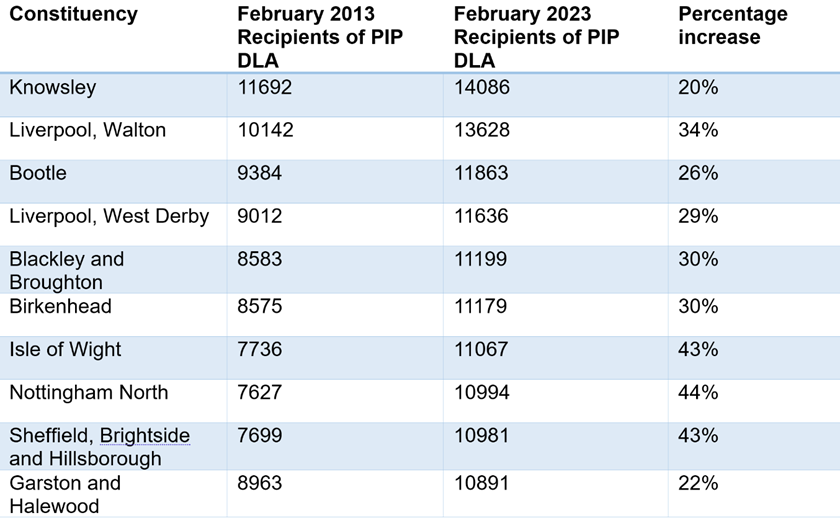

Looking at all PIP / DLA recipients aged 16 or over, receipt of benefits is heavily concentrated in more deprived areas. The table (below) shows the 10 Westminster constituencies with the highest absolute numbers of PIP/DLA recipients as at 2023, and how the number has changed in the last decade. Five of the top six are in the Merseyside area, and all have seen a growth in numbers of 20-30% in the last decade.

If targeted action is not taken, many of the working age claimants in these areas will reach pension age on disability benefits and then be more likely to die in receipt than cease claiming.

Table: Westminster constituencies with largest numbers of 16+ recipients of PIP / DLA in 2023 (England and Wales only)

Source: DWP ‘Stat Xplore’ database

The higher levels of benefit receipt in more deprived areas suggest the potential for targeted health interventions, which could reduce the number of people who need to claim in the first place and/or reduce the length of claim for those who do receive benefits. But, the authors argue government interventions are often insufficiently focused on those most in need. For example:

- The DWP recently expanded its “Individual Placement and Support in Primary Care (IPSPC) programme” designed to support individuals in receipt of disability benefits. However, the list of local authorities chosen to date excludes those where disability benefit receipt is at its highest.

- NHS England has an ‘Elective Recovery Programme’ which aims to increase capacity to tackle the waiting list backlog that worsened materially during the Covid-19 pandemic. Unfortunately, the programme has not specifically prioritised areas of greatest unmet health need.

The paper argues that with each person who reaches pension age on PIP likely to receive another £70,000 in benefit on average, there is great potential for cost-effective interventions which would benefit the individuals concerned as well as the taxpayer. For example:

- Clinically recommended Diabetes meters for those with Type-2 Diabetes cost just £5.50 each; roughly 13,000 such meters could be funded from the savings of just one less person needing PIP through retirement.

- Where people have mental health problems alongside physical problems, low intensity psychological treatments have been demonstrated to be a cost-effective method of treatment. The cost of such ‘collaborative care’ is around £2,140 per person, a fraction of the potential cost saving of £70,000 through avoided benefit payments.

Commenting on the results, co-author and Head of Health Analytics at LCP, Dr Jonathan Pearson-Stuttard said:

“The prospect of large numbers of people going into retirement facing long-term disability benefit receipt is not in the interests of the individuals concerned or the taxpayer. If just one less person needs to claim Personal Independence Payment through retirement the saving is likely to be around £70,000 and that money could be much better spent keeping people well and supporting those who have disabilities. More targeted interventions, particularly focused on areas of greatest deprivation and highest health needs, could pay off many times over in terms of benefit savings and gains to the wider economy.”